使用审计风险模型对审计风险评估系统的研究 The develo.pdf

qw****27

1/10

2/10

3/10

4/10

5/10

6/10

7/10

8/10

9/10

10/10

亲,该文档总共15页,到这已经超出免费预览范围,如果喜欢就直接下载吧~

相关资料

使用审计风险模型对审计风险评估系统的研究 The develo.pdf

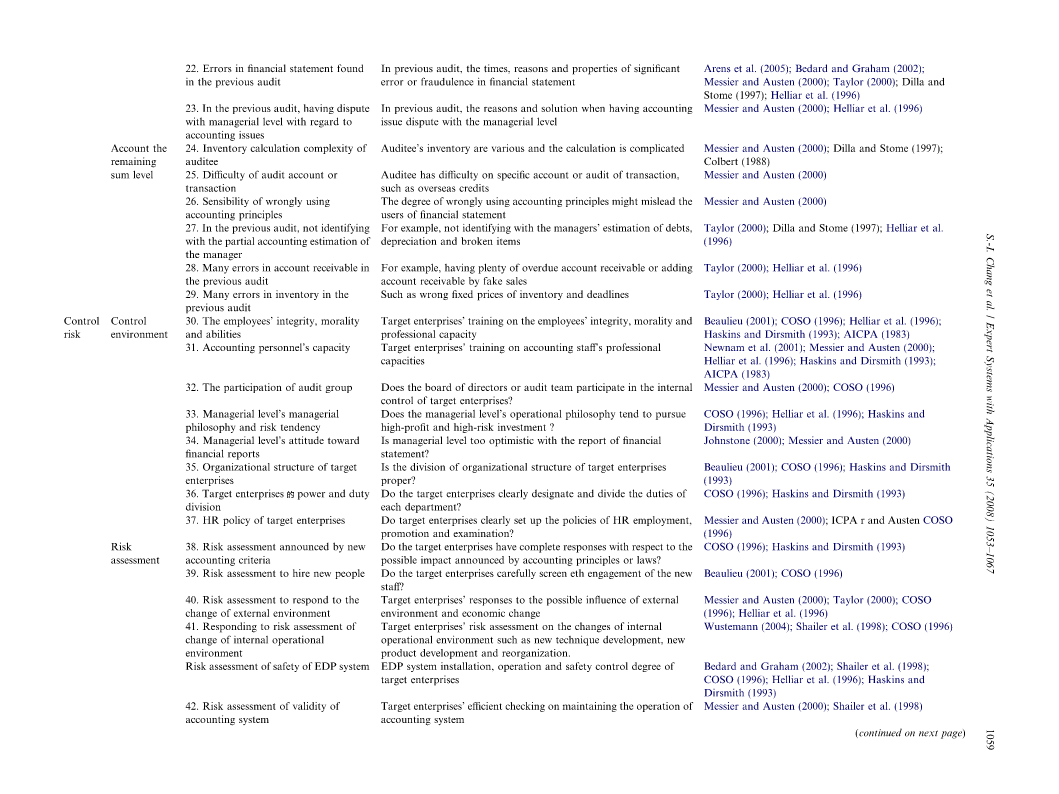

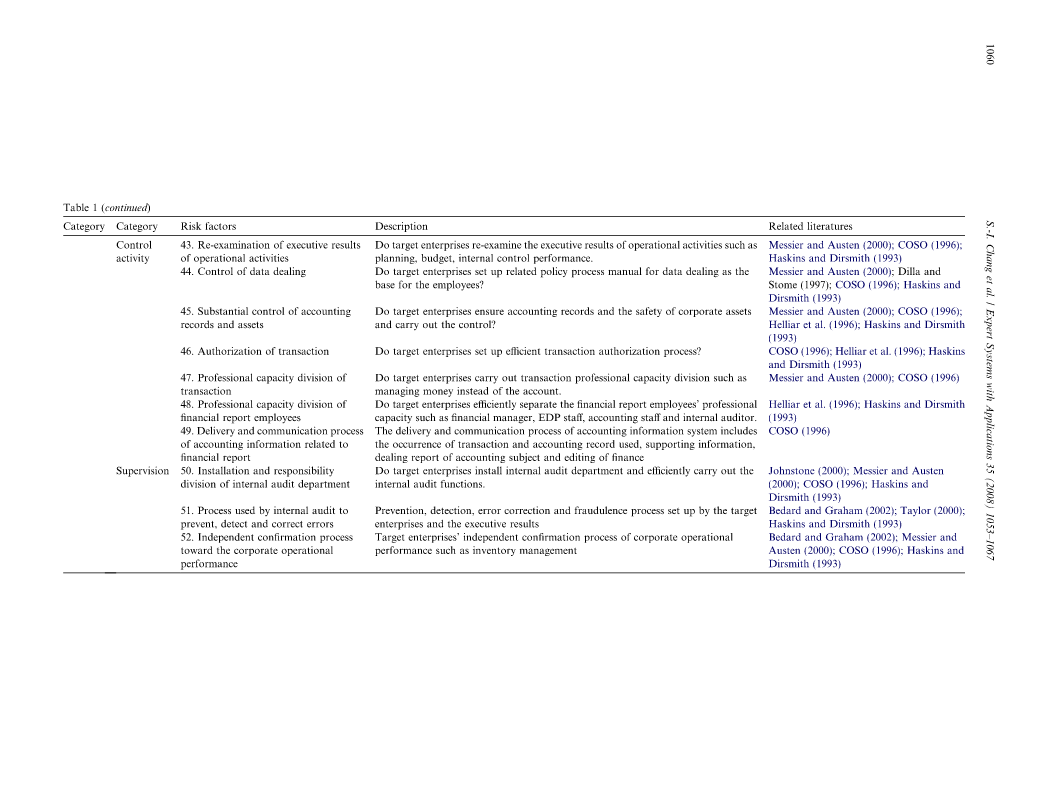

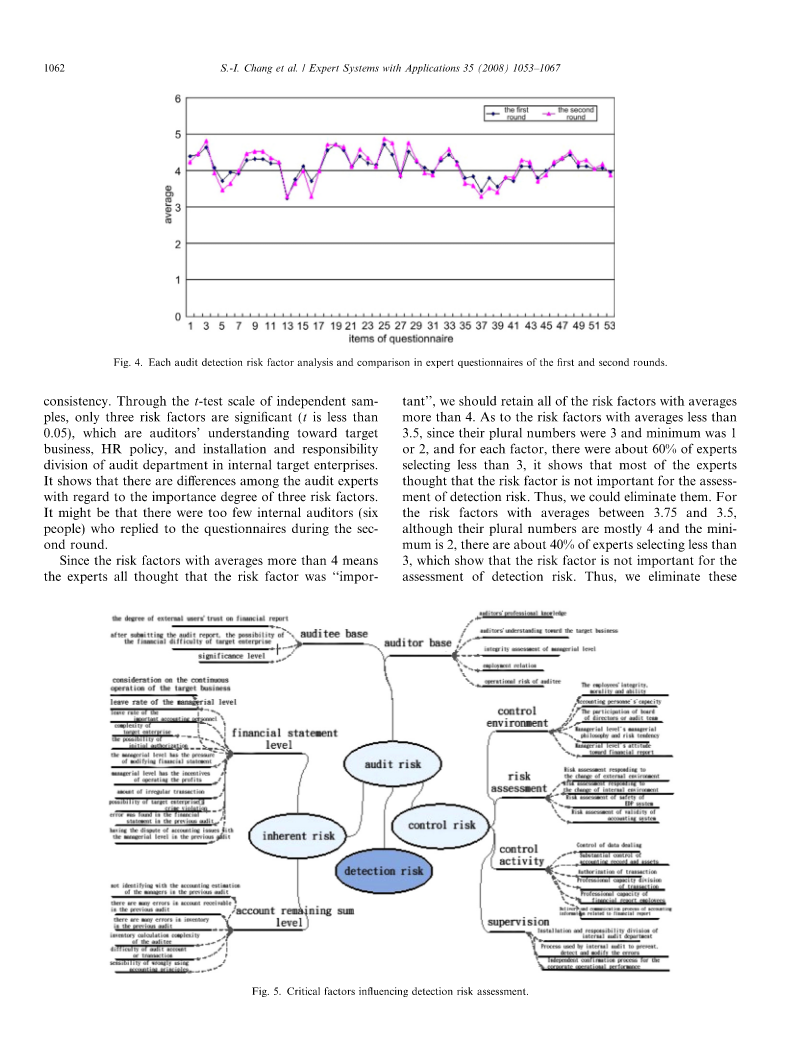

Availableonlineatwww.sciencedirect.comExpertSystemswithApplicationsExpertSystemswithApplications35(2008)1053–1067www.elsevier.com/locate/eswaThedevelopmentofauditdetectionriskassessmentsystem:UsingthefuzzytheoryandauditriskmodelShe-IChanga,*,Chih-FongTsai

高校内部审计风险评估模型研究.docx

高校内部审计风险评估模型研究标题:高校内部审计风险评估模型研究摘要:内部审计对于高校的有效运营和风险管理至关重要。本论文旨在研究高校内部审计风险评估模型,为高校提供有针对性的审计风险管理措施。本文从高校内部审计的定义、目的和重要性入手,介绍了内部审计风险评估的概念和意义,并详细分析了构建高校内部审计风险评估模型的方法和步骤。最后,本文对现有的内部审计风险评估模型进行了综合评价,并提出了进一步研究和应用的建议。关键词:高校内部审计,风险评估,模型研究一、引言高校是培养人才的重要场所,其内部管理和运营面临着各

关于审计风险定义及审计风险模型的研究综述.docx

关于审计风险定义及审计风险模型的研究综述随着社会和经济的发展,企业的规模和复杂性不断提高,这也导致了相应的审计风险的增加。审计风险是指在审计过程中,由于客观因素的存在,可能导致审计师未能发现实际存在的重大差错或欺诈行为的风险。因此,审计风险的管理已经成为了现代审计工作中不可忽视的重要内容。本文将通过综合论述、分析和比较现有的相关文献,对审计风险定义及审计风险模型进行研究和综述。一、审计风险的定义审计风险是指在审计过程中存在的无法避免的、客观存在的风险,包括:控制风险、检查风险和检测风险。其中,控制风险是指

内部审计应用RAROC模型评估企业风险研究.docx

内部审计应用RAROC模型评估企业风险研究随着市场竞争的加剧,企业面临着更为复杂和严峻的风险问题,如何科学有效的评估企业风险,是企业发展的根本保障。内部审计是一种非常重要的企业管理方式,应用RAROC模型评估企业风险,是一种行之有效的内部审计方法。内部审计是指内部组织对企业管理运营进行全面的审计、检查、评估,发现并解决企业存在的风险,提高企业运营效益和风控能力的过程。RAROC模型,即风险调整资本回报率模型,是全球范围内广泛应用的一种风险评估、监测、管理模型。RAROC模型是贷款授信业务和投资决策中通行的

审计风险导向审计及风险评估.pptx

审计(shěnjì)风险导向审计(shěnjì)及风险评估2024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/10/292024/1